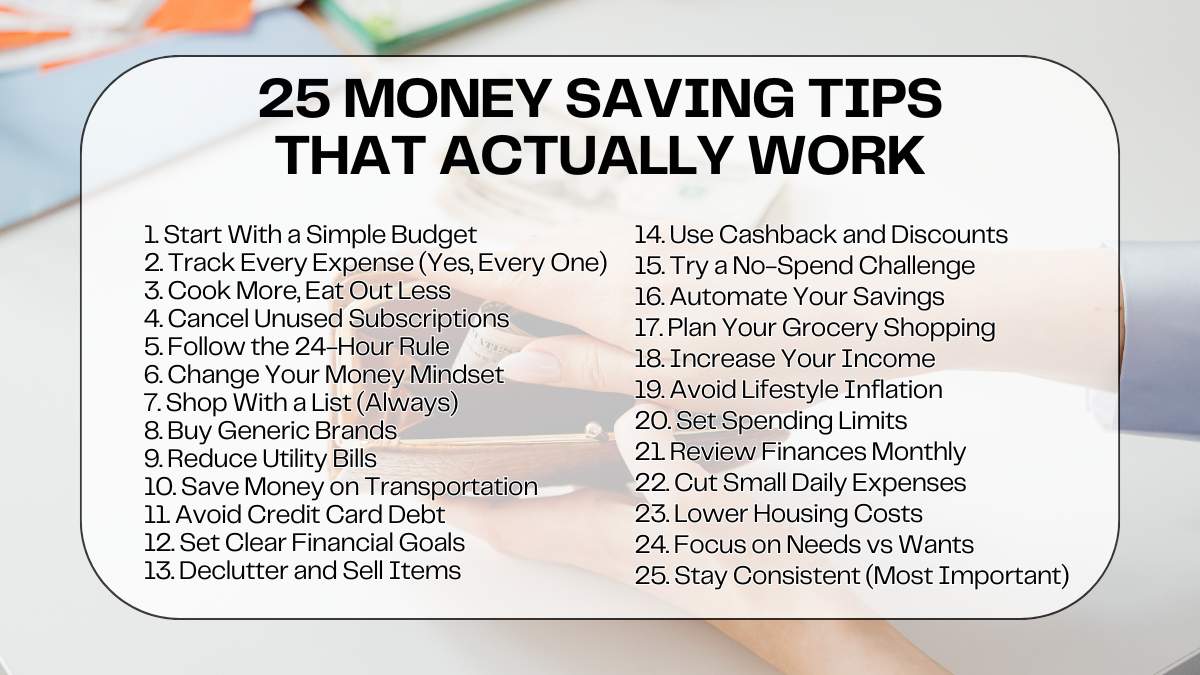

25 Money Saving Tips That Actually Work (Real-Life Ways to Save More in 2026 Without Feeling Broke)

Money saving tips that actually work. That’s what most of us are searching for, right?

Because saving money sounds simple. But in real life? It’s hard. Bills pile up. Small expenses sneak in. And somehow, the paycheck disappears faster than expected.

I’ve been there too. Wondering where my money went. Trying random budgeting tricks that didn’t stick. Feeling frustrated.

But here’s what I’ve learned: saving money doesn’t have to be complicated. It just needs to be realistic.

In this post, I’m sharing 25 money saving tips that actually work—simple, practical strategies you can start today. These are not extreme ideas. No cutting all fun. No unrealistic rules.

Just smart habits. Small changes. Real-life examples.

You’ll find tips on budgeting, cutting expenses, and building better financial habits—all designed to help you save more without feeling stressed.

Because I believe…

Saving money should feel possible, not painful.

💰 1. Start With a Simple Budget

Budgeting sounds boring. I know.

I used to think the same.

But here’s the truth.

A simple budget can completely change your life.

When I first started tracking my money, I felt uncomfortable. Almost shocked.

I finally saw where my money was actually going—not where I thought it was going.

And that changed everything.

A budget is not about restriction. It’s not about saying “no” all the time.

A budget is about awareness.

A budget is about control.

A budget is about freedom.

Why Budgeting Actually Works

Without a budget, money feels random.

You spend here. Spend there.

And at the end of the month… nothing is left.

But when you create a simple plan, something shifts.

You start asking:

- Where should my money go?

- What matters most to me?

- What can I reduce?

That’s where progress begins.

How to Start a Simple Budget

You don’t need anything complicated. No spreadsheets. No fancy tools.

Start simple. Always simple.

Step 1: Write Down Your Monthly Income

Include:

- Salary

- Side income

- Freelance work

Know your total number.

Step 2: List All Expenses

Be honest here. This part matters.

Include:

- Rent

- Groceries

- Bills

- Transportation

- Subscriptions

- Small daily spending

Everything counts.

Step 3: Separate Needs vs Wants

This is where clarity comes in.

Needs:

- Rent

- Food

- Utilities

- Basic transport

Wants:

- Eating out

- Shopping

- Subscriptions

- Entertainment

No judgment. Just awareness.

The Simple 50/30/20 Method

If you feel overwhelmed, use this:

- 50% → Needs

- 30% → Wants

- 20% → Savings

It’s flexible. It’s simple. It works.

👉 Real-Life Example

I once believed I had no extra money.

Every month felt tight.

But when I actually tracked everything…

I found something surprising.

$200 per month was going to small, unnecessary spending.

Coffee here. Delivery there. Random purchases.

Nothing felt big. But together?

It was huge.

The Real Lesson

Small awareness = big change.

Not overnight. Not instantly.

But slowly… consistently…

Everything improves.

🛒 2. Track Every Expense (Yes, Every One)

This step is simple.

But powerful.

Very powerful.

And yes… a little annoying at first.

But stay with me.

Why This Matters So Much

Most people don’t have a money problem.

They have a money awareness problem.

Because the truth is:

👉 Money doesn’t disappear.

👉 It leaks.

And those leaks? They are small.

Very small.

That’s why we ignore them.

Where Money Usually Leaks

Start looking at:

- Coffee runs

- Snacks

- Online shopping

- Subscriptions

- Food delivery

- Small convenience purchases

Individually? No big deal.

Together? A serious problem.

Easy Ways to Track Spending

You don’t need anything fancy.

Keep it simple.

Option 1: Notes App

Write down every expense daily.

Option 2: Budgeting Apps

Apps like:

- Mint

- YNAB

- PocketGuard

Option 3: Weekly Check-Ins

Review your spending every week.

Ask:

- Where did my money go?

- What surprised me?

👉 Real Truth That Changes Everything

Let’s break it down:

- $5 per day

- = $150 per month

- = $1,800 per year

That’s not small anymore.

That’s a vacation. That’s savings. That’s opportunity.

What I Learned Personally

When I started tracking every dollar, I felt uncomfortable.

But also… empowered.

Because now I knew.

And once you know… you can change.

The Real Lesson

Track everything. Even the small things.

Because small things become big things.

🍽️ 3. Cook More, Eat Out Less

Eating out is easy.

Fast. Convenient. Fun.

But expensive.

Very expensive.

The Hidden Cost of Eating Out

You don’t feel it in the moment.

But over time?

It adds up quickly.

I used to eat out without thinking.

Then one day, I calculated everything.

And I was honestly shocked.

Simple Changes That Work

You don’t need to stop completely.

Just reduce.

Try this:

- Cook 3 more meals at home per week

- Meal prep on weekends

- Limit takeout to once per week

Small changes. Big results.

👉 Real-Life Example

Let’s compare:

- $12 lunch × 5 days = $60/week

- Home-cooked meals = $20/week

That’s:

👉 $40 saved per week

👉 $160 saved per month

👉 $1,920 per year

That’s real money.

What Helped Me

I started simple.

Not perfect meals. Not complicated recipes.

Just basic food.

And over time, it became easier.

The Real Lesson

You don’t need to stop enjoying food.

Just be intentional.

Cook more. Spend less.

🧾 4. Cancel Unused Subscriptions

Subscriptions are quiet.

Too quiet.

They don’t feel expensive. But they add up fast.

Why Subscriptions Are Dangerous

Because we forget them.

And they keep charging.

Every month. Automatically.

What to Check

Go through your bank statement.

Look for:

- Streaming services

- Mobile apps

- Gym memberships

- Online tools

- Software subscriptions

Be honest.

Are you really using them?

Action Plan

- Review last 2–3 months of spending

- List all subscriptions

- Cancel anything you don’t use

Keep only what truly adds value.

👉 Real-Life Example

I once reviewed my subscriptions.

I found 4 I wasn’t using.

Canceled them immediately.

Saved $60/month.

That’s:

👉 $720/year

For doing nothing.

The Real Lesson

Subscriptions are small. But powerful.

Control them… or they control your money.

Related: 10 Things You Should Stop Buying to Save Money Fast

🛍️ 5. Follow the 24-Hour Rule

Impulse buying is emotional.

Very emotional.

You see something.

You want it.

You buy it.

Instant.

The Problem

Most purchases are not necessary.

They are reactions.

Not decisions.

The 24-Hour Rule

Simple rule:

👉 Wait 24 hours before buying anything non-essential.

That’s it.

Why This Works

- Reduces emotional spending

- Gives you time to think

- Helps you prioritize

After 24 hours, most urges disappear.

👉 Real-Life Example

I once wanted to buy something for $120.

Felt like I needed it.

Waited one day.

Next day?

Didn’t even care about it anymore.

The Real Lesson

Pause.

Think.

Then decide.

That pause can save you hundreds.

🧠 6. Change Your Money Mindset

Everything starts in your mind.

Everything.

I truly believe this.

Why Mindset Matters

If you believe:

“Saving money is hard”

→ It will feel hard.

If you believe:

“Saving money is possible”

→ You will find ways.

Simple Mindset Shifts

Replace thoughts like:

❌ “I can’t afford this”

✔ “Do I really need this?”

❌ “Saving is painful”

✔ “Saving gives me freedom”

Daily Practices

- Visualize your financial goals

- Track your progress

- Celebrate small wins

Even small progress matters.

What I Learned

Once I changed my mindset, everything became easier.

Not perfect. But better.

The Real Lesson

Your thoughts shape your habits.

And your habits shape your future.

Related: How to Set Financial Goals and Actually Achieve Them

🛒 7. Shop With a List (Always)

This is simple.

Very simple.

But powerful.

Why It Matters

Shopping without a list = overspending.

Always.

You walk in for one thing.

You walk out with ten.

Before You Shop

Do this:

- Write a list

- Stick to it

- Avoid browsing

Discipline matters here.

Bonus Tip (Very Important)

👉 Never shop when hungry.

Seriously.

👉 Real-Life Example

I once went grocery shopping while hungry.

Spent $40 extra.

On things I didn’t need.

The Real Lesson

Plan before you shop.

Because unplanned spending is the biggest enemy of saving money.

Related: $100 Weekly Grocery Budget: Meal Plan + Free Spreadsheet

🧺 8. Buy Generic Brands

Brand names cost more. That’s the truth.

But here’s what many people don’t realize—you’re often paying for the name, not the quality.

I used to think branded products were better. Safer. Higher quality. But once I started comparing… I noticed something surprising.

They were almost the same.

Why generic brands work

Generic (store-brand) products are usually made with similar ingredients and standards. The biggest difference? Marketing and packaging.

You’re not paying for ads. You’re not paying for brand image. You’re just paying for the product.

Try switching in these areas:

- Groceries (rice, pasta, cereal, milk)

- Medicine (pain relievers, vitamins)

- Household items (cleaners, paper towels, detergents)

Simple strategy to start

- Pick 2–3 items you buy regularly

- Try the generic version

- Compare quality and price

👉 Real-life example:

I switched from branded cereal to a store brand. Same taste. Same crunch.

But I saved almost 30% per box.

Why this matters

Saving $2 here. $3 there. It feels small.

But repeat that every week?

That’s hundreds of dollars saved each year.

I believe this:

Smart shoppers don’t chase brands. They chase value.

💡 9. Reduce Utility Bills

Utility bills feel fixed. Like there’s nothing you can do.

But that’s not true.

They are fixed… but still flexible.

Small changes make a big difference over time.

Where your money goes

Most utility bills come from:

- Electricity

- Heating and cooling

- Water usage

And often, we waste more than we realize.

Easy actions that work

Start simple. No need for big changes.

- Turn off lights when leaving a room

- Use energy-efficient LED bulbs

- Unplug devices when not in use

- Wash clothes in cold water

- Take shorter showers

Smarter habits

- Use natural light during the day

- Run appliances only when full

- Set a thermostat schedule

👉 Real-life example:

I lowered my thermostat slightly during winter. Just 1–2 degrees.

I barely noticed the difference. But my bill dropped.

Why this works

Energy companies charge based on usage.

Less usage = lower bills.

A mindset shift

Think of energy like money.

If you waste it, you pay for it.

If you manage it, you save.

Less waste = more savings. Always.

🚗 10. Save Money on Transportation

Transportation is one of those hidden expenses.

Fuel. Maintenance. Parking. Rides. It all adds up fast.

And if you’re not paying attention, it quietly drains your budget.

Where costs come from

- Gas or fuel

- Car repairs

- Insurance

- Ride-sharing apps

Smart ways to save

You don’t need to stop driving completely.

Just drive smarter.

Try this:

- Carpool with coworkers or friends

- Use public transport when possible

- Walk or bike short distances

- Combine errands into one trip

- Avoid unnecessary driving

👉 Real-life example:

I used to make multiple small trips during the week.

Now I combine errands into one day.

Less driving. Less fuel. Less stress.

Bonus tip

Keep your car well maintained.

- Proper tire pressure = better fuel efficiency

- Regular servicing = fewer expensive repairs

The bigger picture

Transportation is necessary. Overspending on it is not.

Think smarter. Not harder.

💳 11. Avoid Credit Card Debt

Credit cards are not bad. But they can become dangerous quickly.

I’ve seen it happen. Small purchases turn into big balances.

And then comes the interest.

Why credit card debt hurts

High interest rates mean:

- You pay more than you borrowed

- Debt grows faster

- Savings slow down

👉 Example:

A $100 purchase can become $150+ with interest.

That’s money lost.

Smart habits to follow

- Always pay your full balance monthly

- Avoid minimum payments

- Don’t spend what you don’t have

A simple rule

If you can’t pay for it in cash…

Don’t put it on a credit card.

Use credit cards wisely

They can still be helpful for:

- Building credit score

- Earning rewards

But only if you stay disciplined.

My mindset

I treat my credit card like a debit card.

No extra spending. No excuses.

Debt slows everything down.

Freedom comes from control.

🎯 12. Set Clear Financial Goals

Saving money without a goal feels… empty.

You save a little. Then stop. Because there’s no reason behind it.

Goals give meaning. Goals give direction. Set Clear Financial Goals.

Why goals matter

They turn saving into something real.

Instead of:

“I should save money”

You say:

“I’m saving for something important”

Examples of financial goals

- Build a $1,000 emergency fund

- Pay off credit card debt

- Save for travel

- Buy a car or home

Make your goals SMART

- Specific – clear target

- Measurable – track progress

- Time-based – set a deadline

👉 Example:

“I will save $1,000 in 5 months by saving $200 each month.”

Why this works

Clarity creates action.

👉 Real-life example:

When I set a clear savings goal, everything changed.

I became more focused. More disciplined.

A simple tip

Write your goal down.

Look at it often.

Purpose creates motivation.

📦 13. Declutter and Sell Items

Look around your home.

How many things do you no longer use?

Probably more than you think.

That’s not clutter.

That’s opportunity.

Turn unused items into cash

You don’t need extra money.

You might already have it.

What to sell

- Clothes you don’t wear

- Old electronics

- Furniture

- Books

- Kitchen items

Where to sell

- Facebook Marketplace

- eBay

- Local selling groups

Simple process

- Clean the item

- Take clear photos

- Set a fair price

- List it online

👉 Real-life example:

I sold old clothes and gadgets I didn’t use anymore. Made over $300.

Bonus benefit

- Less clutter

- More space

- More clarity

Free money from your home.

🛍️ 14. Use Cashback and Discounts

Why pay full price… when you don’t have to?

Smart shoppers don’t just spend. They save while spending.

Easy ways to save

- Use cashback apps

- Apply coupon codes

- Look for sales and deals

- Use reward programs

Before buying anything

- Search for discounts

- Compare prices

- Check cashback offers

👉 Even 5% cashback matters.

Example

Spend $200 → Get $10 back

Repeat this monthly → $120 saved yearly

Stack your savings

- Use coupons + cashback

- Shop during sales

My rule

Never check out without checking for a discount.

It takes 30 seconds. But saves money every time.

Smart shoppers save more. Always.

🧘 15. Try a No-Spend Challenge

This is one of the most powerful habits.

Simple. But life-changing.

A no-spend challenge forces you to reset your habits.

How it works

For a set period:

- No unnecessary spending

- Only essentials allowed

Choose your timeframe

- 7 days

- 14 days

- 30 days

What counts as essential?

- Rent

- Groceries

- Bills

Everything else? Pause.

Why it works

- Breaks bad habits

- Increases awareness

- Helps you reset spending

👉 Real-life example:

I tried a 14-day challenge. I saved more than I expected. But more importantly—I learned where I was wasting money.

What you’ll notice

- You don’t need as much as you think

- Many purchases are emotional

- Saving becomes easier

A simple tip

Make it fun.

- Track your progress

- Set a reward after

Challenge yourself.

You might be surprised by the results.

📅 16. Automate Your Savings

Make saving automatic. No thinking. No stress. No excuses.

This is one of the simplest money habits… but also one of the most powerful. I believe this is where many people finally start seeing real progress.

Because when saving depends on willpower, it often fails. But when it’s automatic? It just happens.

How to set it up:

- Set an auto-transfer from your checking account to your savings account

- Schedule it right after payday

- Start small if needed — even $25 or $50

Try the “Pay Yourself First” system:

Before you spend anything, you save first.

That means:

- Income comes in

- Savings go out immediately

- You live on what’s left

👉 Real-life example:

I started with just $100/month. I didn’t feel it. But after a year? $1,200 saved without effort.

That’s the power.

👉 Out of sight = out of mind.

You don’t miss money you never see.

This works. Every time.

🧾 17. Plan Your Grocery Shopping

Groceries are necessary. Overspending is not.

Food is one of the easiest places to lose money without realizing it. I’ve done it. Many times. Buying random things. Throwing food away. Repeating the cycle.

But once I started planning… everything changed.

Simple grocery planning system:

1. Meal plan weekly

- Choose 5–7 simple meals

- Repeat meals if needed

- Keep it realistic

2. Make a shopping list

- Based only on your meals

- No guessing

- No extras

3. Buy in bulk (smartly)

- Rice

- Pasta

- Frozen foods

- Household basics

4. Avoid food waste

- Use leftovers

- Store food properly

- Don’t overbuy

👉 Real-life example:

Before planning, I spent $400/month. After planning? Around $300.

That’s $100 saved monthly. $1,200 yearly.

Same food. Better system.

Planning is not restrictive. It’s freeing.

💼 18. Increase Your Income

Saving is powerful. But earning more? That’s a game changer.

There’s only so much you can cut. But income? That can grow.

I always say:

Don’t just save your way to wealth. Earn your way too.

Simple ways to increase income:

1. Freelancing

- Writing

- Graphic design

- Data entry

- Social media

2. Side hustles

- Delivery services

- Tutoring

- Online selling

3. Sell your skills

- Photography

- Video editing

- Teaching

👉 You don’t need something big. Start small.

Even:

- $50/month

- $100/month

That extra money can go directly into savings or investments.

👉 Real-life example:

I started a small side hustle that made $150/month. I didn’t spend it. I saved it.

That alone changed my savings speed.

More income = more options.

More options = more freedom.

🧠 19. Avoid Lifestyle Inflation

This is a silent trap.

You earn more… So you spend more.

New phone. Better clothes. More eating out. It feels normal. It feels deserved.

But it slows your financial progress.

What is lifestyle inflation?

When your spending increases as your income increases.

How to avoid it:

- Keep your current lifestyle for a while

- Increase savings when income grows

- Upgrade slowly, not instantly

👉 Example:

You get a $300 raise.

Instead of spending it:

- Save $200

- Use $100 for lifestyle

Balance. Not extremes.

👉 Real-life example:

When my income increased, I didn’t upgrade everything. I kept my habits the same.

Result? I saved more than ever before.

Control your lifestyle. Don’t let it control you.

🎁 20. Set Spending Limits

Limits create awareness.

Without limits, spending becomes emotional. With limits, spending becomes intentional.

I believe everyone should have spending boundaries. Not restrictions. Boundaries.

Simple example:

- $100/month for entertainment

- $50/month for eating out

- $30 for shopping

Once the limit is reached… you stop.

Why this works:

- Prevents overspending

- Builds discipline

- Helps you stay in control

👉 Real-life example:

I set a $50 eating-out limit. Before that, I didn’t even track it.

I was spending $120/month without noticing.

Limits showed me the truth.

Simple rule. Big impact.

📊 21. Review Finances Monthly

You can’t improve what you don’t review.

Checking your finances monthly keeps you aware. It keeps you focused. It keeps you accountable.

I like to think of it as a “money check-in.”

What to review:

- Savings progress

- Monthly spending

- Bills and expenses

- Financial goals

Ask yourself:

- Did I overspend?

- Did I save enough?

- What can I improve next month?

👉 This doesn’t take hours.

Just 15–20 minutes.

👉 Real-life example:

One month I noticed I overspent on food. The next month, I fixed it.

Without reviewing, I wouldn’t even know.

Small check-ins = big improvements.

Consistency wins.

🧃 22. Cut Small Daily Expenses

Small expenses feel harmless.

But they add up fast.

Very fast.

Common daily expenses:

- Coffee

- Snacks

- Drinks

- Apps

- Small online purchases

👉 Let’s break it down:

- $3 per day = $90/month

- $90/month = $1,080/year

That’s not small anymore.

What to do:

- Replace daily coffee with homemade

- Pack snacks from home

- Limit impulse buys

👉 Real-life example:

I reduced my daily spending by $2–$3.

I didn’t feel the difference daily. But yearly? Huge difference.

Small leaks sink big ships.

🏠 23. Lower Housing Costs

Housing is usually your biggest expense.

Even small changes here can save a lot.

This is not always easy. But it’s worth considering.

Ways to reduce housing costs:

- Share rent with a roommate

- Negotiate your rent

- Move to a more affordable area

- Downsize if possible

👉 Example:

Saving $100/month on rent = $1,200/year.

That’s significant.

Think long-term:

Even small housing adjustments can free up money for:

- Savings

- Investments

- Debt payoff

👉 I believe housing decisions shape your financial future more than anything else.

🎯 24. Focus on Needs vs Wants

This is one of the most powerful habits.

And one of the simplest.

Before buying anything, pause and ask:

Do I need this? Or do I just want it?

Needs:

- Food

- Rent

- Utilities

- Basic living expenses

Wants:

- New clothes

- Gadgets

- Dining out

- Entertainment

There’s nothing wrong with wants. But balance is important.

Practice this:

- Delay purchases

- Think before buying

- Prioritize essentials

👉 Real-life example:

I delayed buying something for 2 days. I never bought it.

The urge disappeared.

This mindset alone can save thousands.

🌱 25. Stay Consistent (Most Important)

This is everything.

Not perfection. Not intensity.

Consistency.

I believe this deeply.

What matters most:

- Small steps

- Daily habits

- Repetition

You don’t need to do everything at once.

Start with:

- One habit

- One change

- One goal

Remember:

- Progress takes time

- Results are slow at first

- That’s normal

👉 Real-life truth:

Saving $100/month doesn’t feel big.

But in 1 year = $1,200

In 5 years = $6,000+

Consistency builds momentum.

Consistency builds confidence.

Consistency builds wealth.

Conclusion

Saving money isn’t about being perfect. It’s about being consistent.

These money saving tips that actually work are simple for a reason. Small steps. Repeat them daily. That’s where real change happens.

You don’t need a big income to start. I truly believe that. You can begin with what you have. Even saving a few dollars a week matters.

Over time, those small actions turn into strong financial habits. Less stress. More control. More freedom.

Start with just one or two tips from this list. Try them this week. Keep it simple.

And remember—your financial journey is your own.

💡 If this post helped you, save it on Pinterest or share it with someone who needs these money saving tips too.