Zero-Based Budgeting Guide for Beginners: Take Full Control of Your Money in 2026 (Step-by-Step Plan That Actually Works)

Have you ever opened your bank account and thought, Where did my money go?

I’ve been there. More than once.

Money comes in. Money goes out. And somehow, nothing is left.

I believe the problem isn’t your income. It’s the lack of a clear plan.

That’s where zero-based budgeting comes in.

Simple. Practical. Powerful.

This method gives every dollar a purpose. No guessing. No waste. Just intention.

In this guide, you’ll learn:

- What zero-based budgeting really means

- How to use it in real life

- Why it works better than traditional budgeting

- How it helps you reach your financial goals faster

Let’s make your money work for you.

What Is Zero-Based Budgeting?

Zero-based budgeting sounds technical. But it’s actually very simple.

I like to think of it this way:

Every dollar gets a job.

No money sits around doing nothing. No money disappears.

You tell your money where to go—before it’s gone.

Simple Explanation

Here’s the core idea:

- Your income minus your expenses equals zero

That doesn’t mean you spend everything.

It means you assign everything.

Every dollar is planned:

- Bills

- Groceries

- Savings

- Debt

- Even fun money

Nothing is left unassigned.

Think of It Like This

If you earn $3,000 per month, your budget should look like:

- $3,000 income

- $3,000 assigned

Zero left over.

Zero confusion.

I believe this is what makes zero-based budgeting so powerful.

It forces clarity. It forces intention.

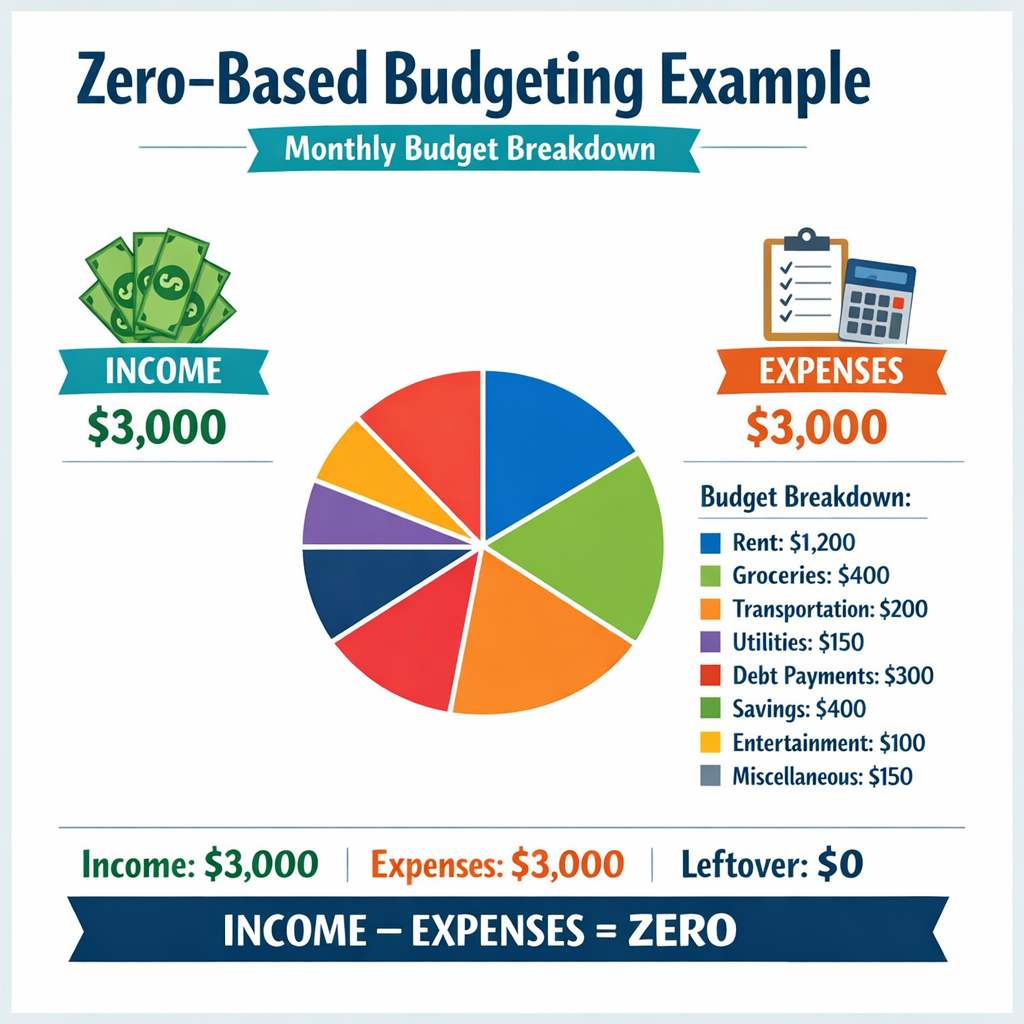

Real-Life Example

Let’s make it real.

Imagine you earn $3,000 per month.

Here’s how a simple zero-based budget might look:

Monthly Budget Breakdown

- Rent: $1,200

- Groceries: $400

- Transportation: $200

- Utilities: $150

- Savings: $400

- Debt payments: $300

- Entertainment: $150

- Miscellaneous: $200

Total = $3,000

Every dollar is assigned.

Nothing is left floating.

Why This Matters

Without a plan, that extra $200 might disappear on:

- Takeout

- Online shopping

- Small daily expenses

But with zero-based budgeting, you stay in control.

You decide first. You spend second.

Related: 30-Day Money Saving Challenge That Works

Why Zero-Based Budgeting Works So Well

Most people don’t fail at budgeting because they’re bad with money. They fail because their system is too loose.

I believe zero-based budgeting works because it removes the guesswork.

It replaces confusion with clarity.

Here’s Why It Works

✔ Gives Full Control Over Your Money

You decide where every dollar goes. Not your habits. Not impulse spending.

You are in charge.

✔ Eliminates Wasteful Spending

When every dollar has a job, overspending becomes obvious.

That random $50 purchase? It now has a cost.

You start asking: Is this worth it?

✔ Helps You Reach Financial Goals Faster

Saving becomes intentional.

Instead of “saving what’s left,” you plan your savings first.

Example:

- $300 goes to savings every month

- Not optional. Not leftover. Planned.

That’s how progress happens.

✔ Creates Awareness of Spending Habits

You start noticing patterns:

- Too much eating out

- Too many subscriptions

- Small expenses adding up

Awareness leads to better decisions.

Better decisions lead to better results.

Related: 15 No-Spend Challenge Ideas That Will Help You Save More in 30 Days

Zero-Based Budgeting vs Traditional Budgeting

Most people already “budget.” But the problem is—they do it loosely.

I’ve seen this many times.

They estimate. They guess. They hope.

And at the end of the month? Confusion again.

Key Differences

Traditional Budgeting

- You estimate your expenses

- You spend as you go

- You save what’s left (if anything)

It feels flexible. But it often leads to overspending.

Zero-Based Budgeting

- You assign every dollar before spending

- You plan everything in advance

- You give your money a clear purpose

Nothing is left unplanned.

Simple Comparison

- Traditional = Reactive

- Zero-Based = Intentional

That’s the difference.

Related: 20 Smart Ways to Cut Monthly Expenses and Save More Money

Which One Is Better for Beginners?

I believe zero-based budgeting is better for beginners.

Why?

Because it removes uncertainty.

Beginners need clarity. They need structure.

Zero-based budgeting provides both.

Here’s Why It Works Better

- It tells you exactly what to do with your money

- It prevents overspending before it happens

- It builds strong financial habits early

Even if you’re just starting your financial journey, this method gives you a clear path.

No confusion. No guessing.

Just a plan that works.

💡 Simple Truth: If you tell your money where to go, you’ll stop wondering where it went.

Related: 25 Money Saving Tips That Actually Work

Step-by-Step Zero-Based Budgeting Plan

Zero-based budgeting is simple. But it works best when you follow a clear system.

I believe structure creates success. Not perfection. Just consistency.

When you break budgeting into small steps, it becomes easier. Less stress. More control.

Let’s walk through this step-by-step plan you can actually follow.

Step 1 – Calculate Your Total Income

Start here. Always start here.

You need to know exactly how much money you have coming in. No guessing. No estimates. Just real numbers.

I used to round numbers. That was a mistake. Small errors create big problems later.

Include All Sources of Income:

- Your main salary (after tax)

- Side hustle income

- Freelance or extra work

- Any passive income

Simple Example:

- Salary: $2,500

- Side hustle: $300

- Total income = $2,800

That’s your starting point.

This number is your foundation. Everything else depends on it.

Step 2 – List All Expenses

Now it’s time to face reality.

This step can feel uncomfortable. I get it. But it’s powerful.

When I first wrote down my expenses, I was surprised. Money was leaking everywhere.

Fixed Expenses (Same Every Month)

These don’t change much:

- Rent or mortgage

- Utilities

- Insurance

- Loan payments

- Subscriptions

Variable Expenses (Change Monthly)

These are flexible:

- Groceries

- Eating out

- Shopping

- Entertainment

- Transportation

Pro Tip:

Go through your last 30 days of spending.

Look at your bank statements. Be honest. Be detailed.

Awareness is everything.

Step 3 – Assign Every Dollar a Job

This is where zero-based budgeting becomes powerful.

Every dollar needs a purpose. No money left “unassigned.”

Income minus expenses should equal zero. That’s the goal.

How It Works:

Take your total income. Start assigning it:

- Rent

- Food

- Bills

- Savings

- Fun money

Keep going until there’s nothing left.

Example:

Income = $2,800

- Rent: $1,000

- Food: $400

- Bills: $300

- Savings: $500

- Spending: $600

Total = $2,800 → Zero left

That’s zero-based budgeting.

You’re telling your money exactly where to go.

Step 4 – Include Savings and Debt Payments

This is where real progress happens.

Savings is not optional. Debt payments are not optional.

I believe this is the biggest shift most people need to make.

Include These Categories First:

- Emergency fund

- Debt repayment

- Investments

Treat them like bills. Non-negotiable.

Real-Life Example:

Instead of saving “what’s left,” you plan it:

- $300 → emergency fund

- $200 → debt payoff

- $100 → investing

You pay your future self first.

That’s how wealth starts. Slowly. Consistently.

Step 5 – Track Your Spending

Your budget is not “set and forget.”

It’s a living plan. It needs attention.

I believe this step is what makes everything work.

Simple Weekly Check-In:

Take 10–15 minutes:

- Review your spending

- Compare with your budget

- Adjust if needed

Why This Matters:

Maybe you spent more on food this week. That’s okay.

Adjust another category. Stay flexible.

Tools You Can Use:

- Budgeting apps

- Simple spreadsheet

- Notebook

Consistency matters more than perfection.

Related: How to Save Money Fast on a Low Income: 21 Simple Tricks That Actually Work

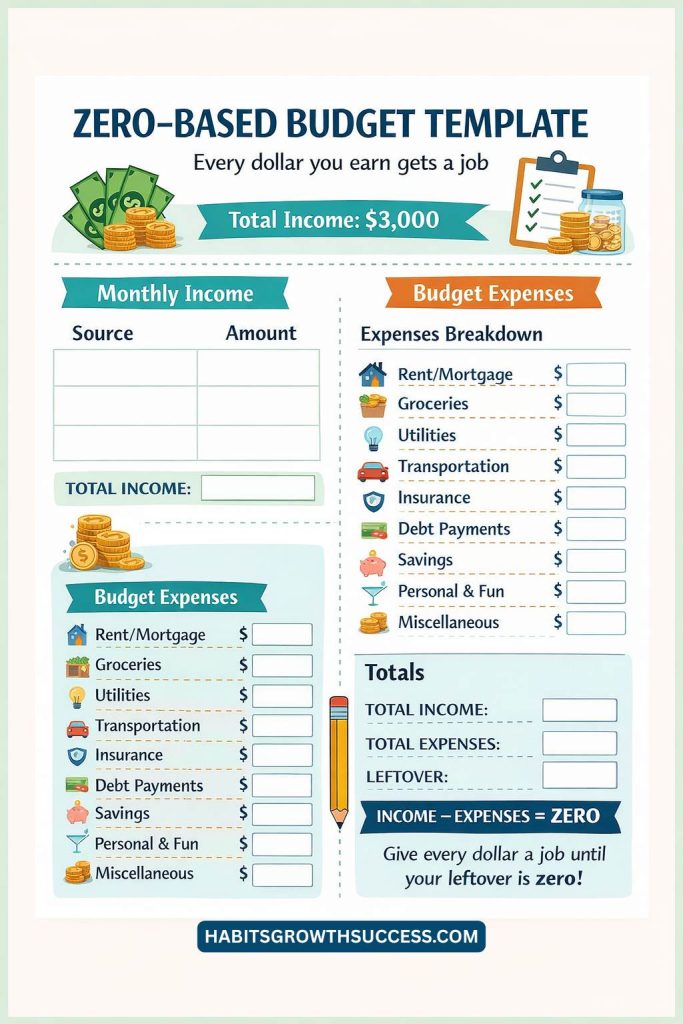

Example of a Zero-Based Budget (Beginner-Friendly)

I believe budgeting becomes easier when you can actually see it. Numbers feel less scary when they are simple. Clear. Organized. Real.

So let’s break it down in a way that makes sense.

Simple Monthly Budget Example

Let’s say your monthly income is $3,000.

Now we give every dollar a job.

Income

- Salary: $3,000

Expenses

- Rent: $1,000

- Groceries: $400

- Transportation: $200

- Utilities: $150

- Insurance: $150

Financial Goals

- Savings: $500

- Debt Payment: $400

Personal Spending

- Entertainment: $100

- Miscellaneous: $100

👉 Total Expenses = $3,000

👉 Money Left = $0

That’s the goal. Every dollar assigned. Nothing wasted.

Why This Works

I like this method because it removes confusion. You don’t wonder where your money went. You already decided where it goes.

Even if your numbers are smaller or bigger, the system stays the same.

Simple. Clear. Repeatable.

Common Mistakes to Avoid

I’ve seen this happen many times. People start strong. Then they get frustrated. Then they quit.

Not because budgeting is hard. But because of small mistakes.

Let’s fix those early.

Forgetting Irregular Expenses

This is a big one.

Things like:

- Car repairs

- Birthdays

- Holidays

- Medical bills

They don’t happen every month. But they will happen.

I always suggest creating a small “extra expenses” category.

Even $50–$100 a month helps.

Being Too Strict

I believe budgets should feel realistic. Not restrictive.

If you cut everything fun, you won’t stick to it.

Example:

- No eating out at all ❌

- No entertainment ❌

That usually fails.

Instead:

- Set a small fun budget

- Enjoy it without guilt

Balance matters.

Not Tracking Spending

A budget without tracking? It doesn’t work.

You need to check:

- Where your money is going

- If you’re staying on track

Even a quick weekly check makes a huge difference.

Awareness changes everything.

Giving Up Too Early

This is the most common mistake.

Your first budget won’t be perfect. Your second might not be either.

That’s normal.

I believe budgeting is a skill. And like any skill, it improves with time.

Adjust. Learn. Continue.

Tips to Make Zero-Based Budgeting Easier

Let’s be honest. Simple systems are the ones that actually work.

If budgeting feels complicated, you won’t stick with it.

So let’s make it easier.

Start Simple

You don’t need a perfect system on day one.

Start with:

- Income

- Bills

- Savings

- Spending

That’s enough.

You can always improve later.

Progress first. Perfection later.

Use Budgeting Apps or Spreadsheets

I believe tools can save time and reduce stress.

You can use:

- Budgeting apps

- Google Sheets

- A simple notebook

Whatever works for you.

The goal is clarity. Not complexity.

Automate Savings

This is one of my favorite tips.

Set up automatic transfers:

- From checking → savings

- Right after payday

You won’t forget. You won’t overspend.

Saving becomes automatic.

Review Your Budget Weekly

This step changes everything.

Just 10 minutes a week.

Ask yourself:

- Am I on track?

- Did I overspend anywhere?

- Do I need to adjust?

Small check-ins prevent big problems.

💡 Simple truth: Budgeting doesn’t have to be hard.

Keep it simple. Stay consistent. Repeat the process.

That’s how real financial progress happens.

Tools to Help You Budget Better

Budgeting is easier when you have the right tools. You don’t need anything complicated. Simple works best.

I believe the goal is not perfection. It’s consistency. The easier your system is, the more likely you’ll stick with it.

Here are a few tools that actually help in real life:

📱 Budgeting Apps

Budgeting apps can make money tracking feel effortless. They do the work for you. They show you the truth.

I’ve seen people completely change their habits just by seeing their spending clearly.

Why they work:

- Automatically track your expenses

- Show spending categories

- Help you stay within your budget

- Send alerts when you overspend

Example:

If you notice you spent $300 on food delivery last month, that awareness alone can help you cut it in half.

👉 Simple tip: Start with one app. Don’t overcomplicate it.

📝 Printable Budget Planners

A printable zero based budget template free download

Sometimes, simple pen and paper works best. Writing things down makes it real. It makes it stick.

I believe there’s power in seeing your numbers on paper.

Why planners help:

- You stay more intentional

- You slow down and think before spending

- You feel more in control

Example:

Each Sunday, write your weekly expenses. This small habit can completely change your awareness.

👉 Tip: Keep your planner somewhere visible. Out of sight = out of mind.

📊 Simple Spreadsheets

Spreadsheets are perfect if you like structure.

Clean. Clear. Organized.

They give you a full picture of your money.

What you can track:

- Income

- Fixed expenses

- Variable spending

- Savings progress

Example:

A simple Google Sheet with categories like rent, food, and savings can help you see exactly where your money goes.

👉 Tip: Review your budget weekly. Just 10 minutes. That’s enough.

How Zero-Based Budgeting Helps You Reach Financial Goals

Zero-based budgeting is not just about tracking money. It’s about building a better financial life. Every dollar has a purpose. Every decision becomes intentional.

I believe this is where real change happens.

Let’s look at how it helps you move forward.

💰 Builds Savings Habits

Saving becomes automatic. Not optional.

When you assign money to savings first, you stop relying on “leftover money.”

Example:

Instead of saving what’s left, you plan to save $200 first. Every month. No excuses.

👉 Tip: Treat savings like a bill. Non-negotiable.

💳 Reduces Debt Faster

Debt doesn’t disappear by accident. It disappears with a plan.

Zero-based budgeting forces you to face your numbers. And that’s powerful.

Example:

If you assign an extra $150 monthly to debt, you speed up your payoff timeline significantly.

👉 Tip: Focus on one debt at a time for faster progress.

🧠 Improves Money Mindset

You start thinking differently. You become more aware. More intentional.

I believe mindset is everything in personal finance.

Instead of asking: “Can I afford this?”

You start asking: “Is this worth it?”

👉 That shift changes everything.

📈 Supports Long-Term Wealth

Wealth is built slowly. Consistently. Intentionally.

Zero-based budgeting helps you:

- Invest regularly

- Save consistently

- Avoid unnecessary debt

Example:

Even investing $100 monthly can grow into something powerful over time.

👉 Tip: Think long-term. Small steps today create big results later.

Who Should Use Zero-Based Budgeting?

The truth is simple. This method works for almost everyone. But for some people, it can be life-changing.

I’ve seen it work again and again.

👶 Beginners

If you’re new to budgeting, this is a great place to start.

It’s simple. Clear. Easy to follow.

You don’t need financial knowledge. You just need a plan.

👉 Tip: Start with your monthly income and build from there.

💸 People Living Paycheck to Paycheck

If money feels tight every month, this method can help.

It shows you exactly where your money is going. And where you can make changes.

Example:

Cutting just $5–$10 daily expenses can free up hundreds per month.

👉 Small changes matter. More than you think.

🎯 Anyone Wanting Better Money Control

If you feel like your money disappears… this is for you.

Zero-based budgeting gives you control.

Clear. Simple. Powerful.

I believe everyone deserves to feel confident about their money.

👉 Tip: Start small. Progress matters more than perfection.

Final Thoughts

Budgeting doesn’t have to be hard. It doesn’t have to feel restrictive.

It can feel empowering.

I believe anyone can improve their finances with simple steps. You don’t need to be perfect. You just need to start.

Small steps lead to big results. One decision at a time. One habit at a time.

Start today.

- Write down your income

- Plan your expenses

- Give every dollar a job

And most importantly…

👉 Review your budget weekly.

Just a few minutes each week can keep you on track and moving forward.

Your future self will thank you.